It’s May 14, 2025, and the financial landscape is evolving faster than ever. Open banking, a concept that once seemed like a futuristic dream, is now a reality reshaping the way merchants do business. From small online stores to large retail chains, businesses are tapping into the power of open banking to streamline operations, cut costs, and enhance customer experiences. If you’re a merchant or simply curious about the future of payments, let’s explore how open banking is transforming merchant services this year and what it means for the road ahead.

Understanding Open Banking: A Quick Primer

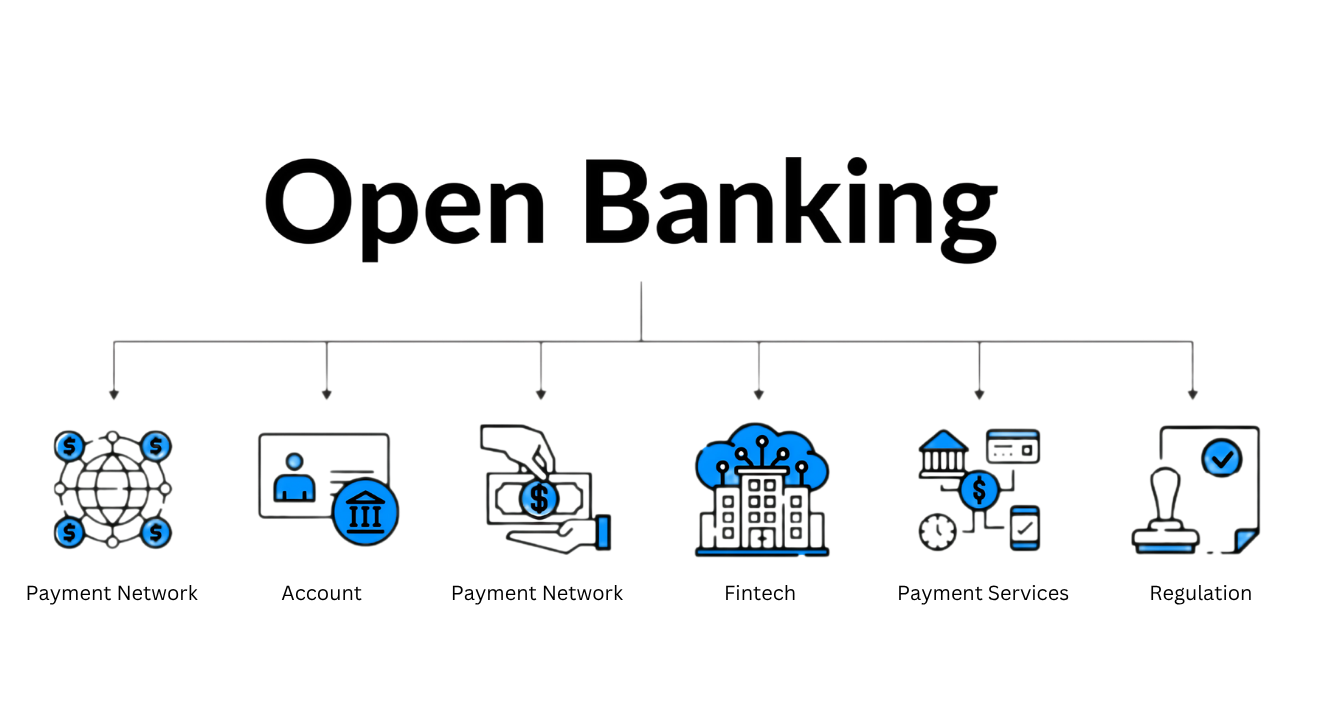

First things first—what exactly is open banking? In simple terms, it’s a system where banks share customer financial data with third parties, like fintech apps or merchants, through secure APIs (application programming interfaces). This sharing happens only with the customer’s explicit consent, ensuring privacy and security. The goal? To create a more connected, efficient financial ecosystem.

Picture this: you’re buying a pair of shoes online, and instead of pulling out your credit card, you opt to pay directly from your bank account. With open banking, the merchant can securely access your account to payment processing instantly—no card, no hassle. In 2025, this seamless process is becoming the standard, and merchants are reaping the benefits in a big way.

Cutting Costs with Pay-by-Bank Solutions

One of the most significant ways open banking is redefining merchant services in 2025 is through the rise of pay-by-bank options. This payment method allows customers to transfer money directly from their bank accounts to the merchant, bypassing traditional card networks like Visa or Mastercard. For merchants, this is a game-changer because it slashes transaction fees.

Card payments typically come with fees of 2-3% per transaction, which can eat into a merchant’s profits, especially for small businesses. Pay-by-bank transactions, enabled by open banking, often have much lower fees—or none at all in some cases. Imagine a local coffee shop that processes hundreds of transactions daily. By switching to pay-by-bank, they could save thousands of dollars annually, money that can be reinvested into the business.

Beyond cost savings, these payments are lightning-fast. In 2025, instant bank transfers are the norm, meaning merchants don’t have to wait days to receive funds. This improved cash flow is a lifeline for businesses with tight margins, allowing them to manage inventory, pay suppliers, and grow without delay.

Customers love it too. With security features like two-factor authentication and biometric verification, pay-by-bank transactions are safer than ever. In a time when data breaches make headlines, this added layer of protection is a major selling point for both merchants and shoppers.

Enhancing Customer Experiences Through Data Insights

Open banking isn’t just about payments—it’s also unlocking new ways for merchants to connect with their customers. In 2025, businesses are using the financial data shared through open banking to create more personalized shopping experiences. This isn’t about snooping; it’s about using consented data to understand customer needs better and offer tailored solutions.

For example, let’s say you own a pet store. Through open banking, you can see (with permission) that a customer has been spending a lot on premium pet food. Armed with this insight, you might suggest a subscription plan for organic dog treats, increasing the likelihood of a sale. This level of personalization was once reserved for big players with massive marketing budgets, but now even small merchants can get in on the action.

This trend is particularly impactful in industries like fashion, travel, and dining, where knowing a customer’s preferences can make all the difference. In 2025, merchants who use open banking data to personalize their offerings are seeing higher engagement, better conversion rates, and more repeat customers. It’s a simple equation: when customers feel understood, they’re more likely to stick around.

Streamlining E-Commerce with Seamless Checkouts

If you’ve ever abandoned an online shopping cart because the checkout process was too complicated, you’re not alone. In 2025, open banking is tackling this pain point head-on by simplifying e-commerce transactions. Pay-by-bank solutions allow customers to authenticate and pay directly through their banking app, often with just a couple of taps.

Compare this to traditional card payments, where you might need to enter a 16-digit card number, expiry date, and CVV, then wait for a verification code. It’s no wonder cart abandonment rates have historically been high. With open banking, the process is streamlined, reducing friction and making it easier for customers to complete their purchases.

For merchants, this means fewer lost sales. In 2025, e-commerce giants and small businesses alike are adopting pay-by-bank options to keep customers happy and boost their bottom line. This is especially true for high-value purchases, like electronics or luxury goods, where customers value the speed and security of direct bank payments.

That said, it’s not all perfect. Refunds for pay-by-bank transactions can be tricky, as the process isn’t as standardized as it is for card payments. Some merchants are using workarounds, like issuing refunds through digital wallets, but it’s an area that still needs improvement. Despite these challenges, the benefits of smoother checkouts are undeniable, and open banking is leading the charge.

Empowering Small Merchants with Financial Tools

Small and medium-sized businesses (SMEs) have often struggled to compete with larger players, but open banking is leveling the playing field in 2025. By providing access to real-time financial data, open banking is helping SMEs manage their finances more effectively. For instance, fintech tools can now analyze a merchant’s cash flow and automatically move funds between accounts to avoid overdraft fees or optimize savings.

Access to financing is another area where open banking is making a difference. In the past, getting a business loan could take weeks, with endless paperwork to prove creditworthiness. Now, lenders can use open banking data to assess a merchant’s financial health in real time, speeding up the process. For a small retailer needing funds to stock up for the holiday season, this quick access to capital can be a game-changer.

The Role of Regulation in Driving Change

Open banking wouldn’t be where it is in 2025 without strong regulatory support. In the U.S., the Consumer Financial Protection Bureau (CFPB) has implemented the Personal Financial Data Rights rule, which mandates that banks share customer data with third parties upon request, at no cost to the customer. This rule, which started rolling out this year, is giving merchants the confidence to adopt open banking solutions, knowing there’s a clear framework in place.

In Europe, the Third Payment Services Directive (PSD3) is further advancing open banking by enhancing security and standardizing processes across the region. These regulations are fostering trust and encouraging more merchants to embrace open banking, knowing that both they and their customers are protected.

Challenges to Overcome

Despite its promise, open banking isn’t without hurdles. One of the biggest is consumer trust. Many people are still wary of sharing their financial data, even with consent, due to fears of misuse or breaches. Merchants and fintechs will need to prioritize transparency and education, showing customers the robust security measures—like encryption and multi-factor authentication—that safeguard their data.

Another challenge is the need for collaboration. Open banking works best when banks, fintechs, and merchants work together seamlessly, but aligning these stakeholders can be complex. In 2025, we’re seeing more partnerships emerge, but there’s still work to be done to ensure a cohesive ecosystem.

Looking to the Future

As we move further into 2025, the impact of open banking on merchant services is only going to grow. We can expect even more innovation, from AI-powered financial insights to deeper integrations with digital wallets and loyalty programs. For merchants, staying ahead means embracing these changes and finding ways to use open banking to their advantage.

Conclusion In 2025, open banking is redefining merchant services in ways that were unimaginable just a few years ago. From reducing costs and streamlining payments to offering personalized experiences and empowering small businesses, this technology is transforming the way merchants operate. While challenges like consumer trust and collaboration remain, the opportunities are immense. For merchants who adapt, open banking isn’t just a trend—it’s a pathway to a more efficient, customer-centric future. The financial world is open, and merchants are ready to thrive.