For decades, checks symbolized trust in financial transactions. Handwritten, signed, and carried to the bank — they represented the physical proof of a deal between two parties. But in 2026, this once-paper-bound method has transformed into something faster, smarter, and completely digital.

Welcome to the age of eCheck payment processing, where paper has turned into pixels — and financial efficiency meets advanced technology.

As the digital economy matures, eCheck and ACH payments have become the backbone of secure, low-cost, and instant transactions. Businesses across sectors — from SaaS and healthcare to logistics and education — now rely on accepting eCheck payments to reduce costs and speed up cash flow.

This blog explores how the humble check evolved into a powerful digital solution, what’s driving its widespread adoption, and how 2026 is redefining the way we move money.

1. A Brief History: From Paper Trails to Digital Rails

The story of eChecks begins in the early 2000s when financial institutions first experimented with digitizing the check clearing process. But the real transformation began when the Check Clearing for the 21st Century Act (Check 21) was implemented in the United States in 2004.

This allowed banks to process digital images of checks instead of physical paper. Over time, as ACH (Automated Clearing House) systems advanced, checks evolved into fully electronic transactions — giving birth to what we now call eChecks.

Fast-forward to 2026, and paper checks have nearly vanished in many sectors. Businesses and consumers now prefer eCheck and ACH payment processing for their reliability, low fees, and ease of integration with digital platforms.

2. The 2026 Landscape: Why eChecks Are Thriving

In today’s fast-paced economy, efficiency rules. The rise of digital-first banking, AI-powered payment gateways, and regulatory modernization has pushed eChecks into the mainstream.

According to a 2025 NACHA report, over 7 billion ACH payments processed in the U.S. originated from eCheck authorizations — a 35% increase over 2023.

So, what’s driving this shift?

- Lower Costs: eCheck transactions cost up to 80% less than credit card processing.

- Enhanced Security: Advanced encryption and tokenization make eChecks safer than ever.

- Instant Settlements: With Same Day ACH and FedNow integrations, most transactions clear in minutes.

- Regulatory Confidence: NACHA and the Federal Reserve maintain strong compliance frameworks, ensuring reliability.

- Global Compatibility: Cross-border eCheck processing is emerging as a fast, low-cost international payment solution.

The combination of speed, cost, and trust makes eCheck processing an unbeatable option for modern businesses.

3. The Technology Behind eChecks

Today’s eCheck is far more than a digital image — it’s a secure, data-encrypted payment protocol designed for instant authentication and settlement.

Let’s break it down:

- Authorization: A payer authorizes the transaction online (through a secure portal, email, or API).

- Data Encryption: Banking details are tokenized and encrypted using AES-256 protocols.

- Transmission: The payment data travels through the ACH network.

- Verification: AI systems validate the transaction, ensuring account legitimacy and fraud protection.

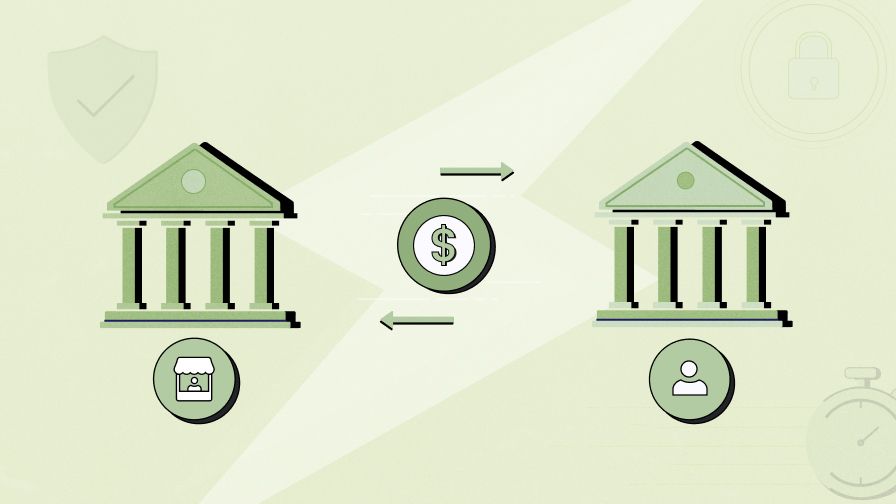

- Settlement: Funds move directly between verified bank accounts — often within hours.

This level of automation and intelligence ensures that businesses can accept ACH payments instantly without compromising on compliance or security.

4. From Slow to Swift: Speeding Up Digital Settlements

One of the biggest milestones for ACH and eCheck payments in 2026 is the rise of real-time settlement networks.

Just a few years ago, eCheck deposits could take 2–3 business days to clear. Today, with Same Day ACH, FedNow, and AI-driven transaction verification, businesses can receive cleared funds in under 60 minutes.

This evolution impacts every industry:

- E-commerce: Instant refunds and payment confirmations enhance customer satisfaction.

- Subscription Models: Recurring billing becomes faster and error-free.

- B2B Transactions: Companies no longer wait days to reconcile invoices.

Speed has officially caught up with trust — and it’s redefining how money moves.

5. Security in 2026: The Core of Digital Trust

As payment speed increases, so does the importance of security. Businesses must ensure that rapid processing doesn’t open doors to fraud or data theft.

In 2026, leading eCheck processors deploy multi-layered protection systems, including:

- Tokenization: Replacing sensitive bank data with unique digital tokens.

- AI Fraud Monitoring: Identifying irregular payment behaviors in real time.

- Two-Factor Authentication: Strengthening user identity verification.

- Blockchain Verification: Creating immutable transaction records for transparency.

- Regulatory Compliance: Adhering to NACHA’s strict security standards and data protection protocols.

The result? eCheck payment processing has become one of the most secure digital payment methods — even surpassing cards in certain risk metrics.

6. The Rise of AI in Payment Processing

AI isn’t just improving fraud detection — it’s redefining the entire eCheck ecosystem.

Modern processors now integrate AI at multiple levels:

- Smart Routing: AI chooses the fastest and most cost-efficient payment path.

- Predictive Risk Scoring: Real-time risk profiles are created for each transaction.

- Automated Reconciliation: Machine learning ensures that all payments are accurately matched with invoices.

- Voice-Enabled Payments: Voice AI assistants can now initiate and verify eCheck payments for businesses.

By combining AI and eCheck payments, companies gain not just speed and savings — but also intelligent automation that reduces manual intervention.

7. How Businesses Are Adapting to Digital eChecks

The shift from paper to pixels is evident in every business segment. From local service providers to multinational enterprises, the appeal of eCheck and ACH payments for business lies in flexibility and scalability.

Industries Leading the Charge:

- Healthcare: Automated billing and patient payment solutions powered by ACH.

- Insurance: Instant premium collections through secure eCheck authorization.

- Education: Digital tuition payments with recurring eCheck options.

- Real Estate: Landlords automating rent collection and deposits.

- SaaS Companies: Seamless recurring billing via direct bank transfers.

In 2026, even small businesses can accept electronic check payments through simple API integrations, mobile apps, or payment gateways — without needing complex banking setups.

8. Environmental Impact: Sustainability Through Digital Finance

The transition from paper checks to eChecks isn’t just about convenience — it’s also a victory for sustainability.

Consider this: every year, over 13 billion paper checks were printed in the U.S. alone, consuming millions of pounds of paper and ink.

By moving to eCheck payment processing, businesses help:

- Save trees and reduce deforestation.

- Eliminate the carbon footprint of postal delivery.

- Cut down on plastic waste from traditional payment cards.

In short, eChecks are the eco-friendly evolution of financial transactions — merging digital efficiency with environmental responsibility.

9. The Role of Regulation and Compliance

Strong regulation has always been the backbone of trust in banking systems. In 2026, eCheck and ACH compliance frameworks are stronger than ever.

NACHA, the governing body of the ACH network, has implemented several new measures:

- Mandatory Account Verification: Ensures both payer and payee accounts are valid.

- Same Day ACH Standardization: Enables universal near-instant settlements.

- Fraud Prevention APIs: Standardized APIs for banks and processors to share risk data securely.

- Enhanced Data Privacy: Compliance with global standards like GDPR and CCPA.

These rules not only protect consumers but also allow businesses to accept ACH payments securely and stay fully compliant with minimal administrative overhead.

10. Global Expansion: The Cross-Border Future of eChecks

In 2026, the next frontier for eChecks is international payments.

Traditionally, global transactions relied on expensive wire transfers or SWIFT networks. But with emerging fintech partnerships, cross-border ACH systems are now connecting seamlessly between countries.

This enables businesses to:

- Receive international eCheck payments at lower fees.

- Process cross-border transactions in under a day.

- Expand global customer bases without payment friction.

For example, U.S.-based merchants can now accept eChecks from customers in Canada, the UK, and India, thanks to network interoperability and blockchain-backed validation systems.

11. Challenges: What’s Still Holding eChecks Back

While eChecks have evolved rapidly, a few challenges remain:

- Awareness Gap: Many consumers still don’t fully understand eCheck systems.

- Bank Integration: Smaller banks may lag in supporting real-time ACH features.

- Business Adoption Costs: Some merchants hesitate due to initial integration expenses.

- Fraudulent Onboarding: Fake account setups remain a potential risk without strict KYC.

However, these challenges are being actively addressed through education, AI identity verification, and fintech innovation, ensuring that eChecks continue to grow in adoption and reliability.

12. What’s Next for eChecks and ACH Payments

As we look toward 2027 and beyond, three major trends define the future of eCheck payment processing:

- Hyper-Automated Payment Ecosystems: AI-driven workflows that manage the entire payment lifecycle — from authorization to reconciliation.

- Embedded Payments: Businesses integrating eCheck and ACH directly into websites, CRMs, and ERP systems.

- Blockchain Ledger Integration: Transparent, tamper-proof tracking of every eCheck transaction.

The combination of these innovations will make ACH and eCheck payments not only faster and safer but also context-aware — adapting dynamically to user behavior and business needs.

13. Strategic Takeaways for Businesses

By 2026, the financial winners are those who blend efficiency with trust.

Here’s how businesses can stay ahead:

- Integrate eCheck Payments: Use platforms that allow instant authorization and eCheck deposit automation.

- Focus on Security: Choose processors with multi-layer encryption and AI fraud analytics.

- Leverage Analytics: Use payment data to forecast revenue and improve financial planning.

- Offer Flexible Options: Let customers choose between ACH, eCheck, and real-time bank transfers.

When you accept eCheck payments, you’re not just improving transactions — you’re building a foundation for sustainable, scalable growth.

14. From Paper Legacy to Digital Future

The journey from paper checks to digital eChecks reflects the broader evolution of the financial world — from manual and fragmented to intelligent and seamless.

In 2026, eCheck payment processing represents more than just a payment method. It’s a statement of efficiency, trust, and progress.

By embracing this technology, businesses not only simplify transactions but also future-proof their operations against the ever-changing demands of the digital economy.

As finance continues to move from paper to pixels, eChecks stand as a symbol of transformation — merging the credibility of traditional banking with the innovation of modern fintech.

The message for 2026 is clear:

The future of payment is direct, digital, and dependable — and eChecks are leading the charge.