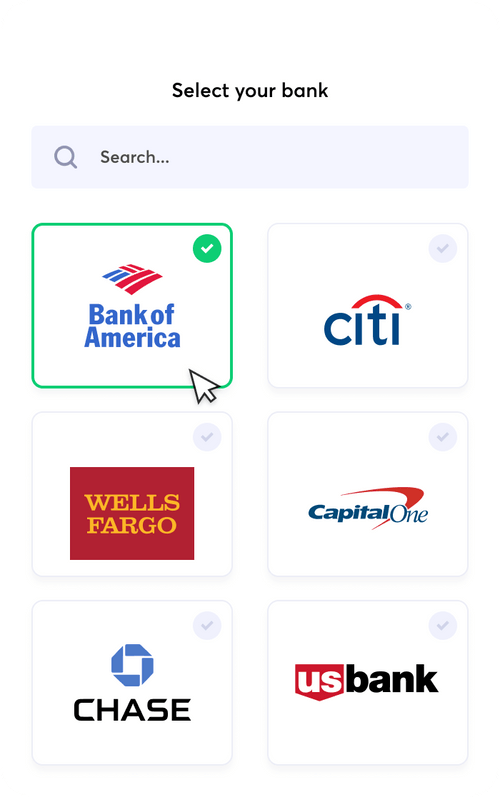

The recipient selects their financial institution

The recipient enters online bank credentials

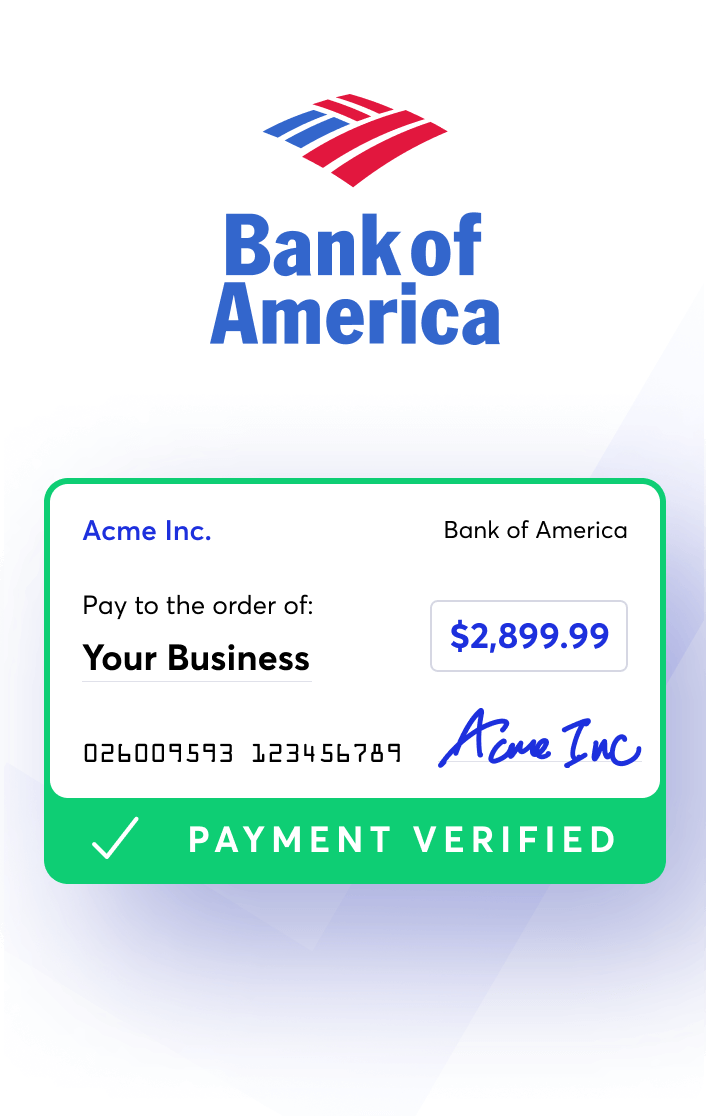

The recipient 's bank account is verified

Instant Bank Verification

Payment Links and Online Checkout

Recurring Billing

Store Payment Methods

Developer Friendly API

White Label Solutions

Streamlined Financial Solutions for Freelancers and Self-Employed Individuals

Efficiently dispatch invoices and online payments to clients or vendors without the need for credit checks or elaborate bank underwriting processes. Discover the convenience and cost-effectiveness of iPay Digital, providing budget-friendly pricing solutions designed to save you time and money.

Take your agency or small business to new heights with enhanced efficiency and streamlined processes.

Facilitate payments for clients, vendors, contractors, landlords, or any other stakeholders effortlessly. Utilize our state-of-the-art verification tools to ensure the availability of client funds prior to initiating payments. Simplify your financial management with iPay Digital's robust payment tracking system.

Debit bank accounts via eCheck and ACH

Effortlessly debit bank accounts with the convenience of eCheck and ACH transactions

Accept Verified ACH payments

Safely and seamlessly accept verified ACH payments for enhanced transaction security

Accept Debit and Credit Card payments

Enable smooth business transactions by effortlessly accepting both debit and credit card payments